M&A in Renewable Energy: France and the UK at the Heart of European Consolidation

M&A in Renewable Energy: France and the UK at the Heart of European Consolidation

Since 2019, the renewable energy landscape has been undergoing a profound transformation. The sector has been driven by a surge in mergers and acquisitions (M&A) activity. These transactions now represent much more than mere growth levers — they have become strategic tools for portfolio optimization and capital allocation. In this evolving context, France and the United Kingdom occupy a central position, supported by the maturity of their markets, the quality of their assets, and a regulatory environment conducive to investment.

2019: A Landscape Still Dominated by Greenfield Projects

In 2019, development strategies in France and the UK were still primarily based on greenfield projects. Developers favored project creation to meet market demand and national and European renewable energy targets. At that time, Greensolver notices that M&A activity remained marginal in both countries, unlike markets such as Italy and Spain, where acquisitions emerged as faster growth drivers. This contrast reflected differing maturity levels across the European market.

2020: The UK Leads Renewable M&A, France Begins Its Shift

This year marked a turning point in Europe, Greensolver was involved in multiple M&A deals during the year. The UK recorded nearly €460 million in renewable energy transactions, driven by growing interest from investment funds and institutional players. Greensolver observes that offshore wind attracted capital thanks to the depth of the market and the UK’s favorable geographic position for marine projects. In parallel, France began to structure its operational portfolios, in turn attracting new investors seeking stable and profitable assets. This marked the beginning of a consolidation phase that would intensify in the years ahead.

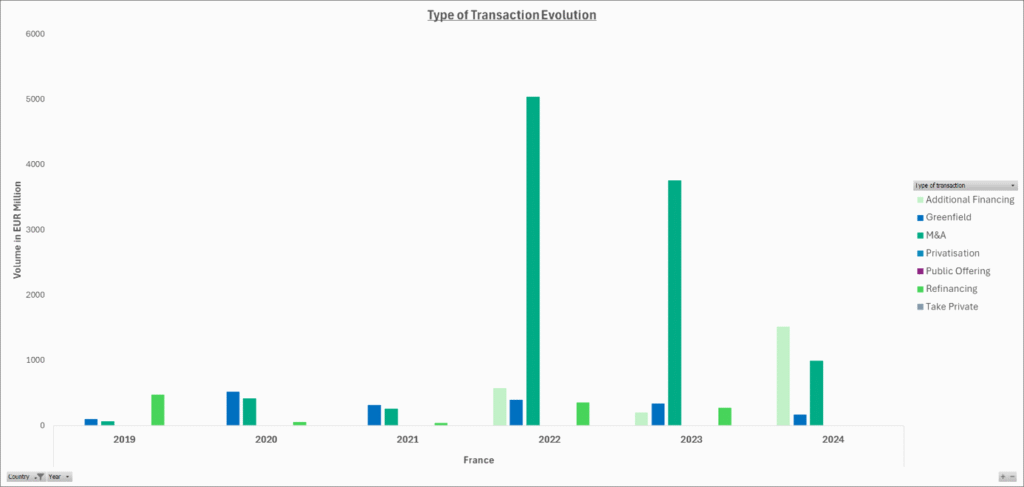

2021–2023: A Structured Market Led by France and the UK

During this period, the European market entered a clear phase of consolidation. France stood out in 2022 with a transaction peak of €5.05 billion, a significant portion of which was facilitated by Greensolver. This wave of consolidation was driven by increasingly complex operations: acquisitions of operating portfolios, brownfield projects, vertical integration of developers, and structured refinancings. The UK, for its part, continued its momentum, relying on a robust set of mature assets and a favorable regulatory framework. While the UK market focused on offshore wind (with a peak of Greenfield projects in 2023) and storage, the French market was driven by solar projects, highlighting a shared level of market maturity.

Toward New European Equilibriums

While France and the UK continue to refine their positioning through M&A activity, other European countries are following different trajectories. Greece, Poland, and Romania remain focused on greenfield developments, reflecting ambitious public policies and a strong need for new installed capacity.

In both France and the UK, greenfield projects remain present, though most are now part of broader aggregation strategies. These projects are integrated into larger portfolios, aimed at resale or institutional structuring. Today, Greensolver points out that solar, wind, and storage solutions have become strategic segments, at the crossroads of technological innovation and financial optimization.

2025 Outlook: Financial Structuring and Innovation as Growth Drivers

M&A in renewable energy is now established as a strategic lever for capital allocation. In both France and the UK, sector players (developers, funds, utilities) are moving toward hybrid models, combining greenfield development, acquisition of mature assets, and mastered financial structuring.

The emergence of flexibility solutions (BESS and hybrid systems) is also opening new opportunities, particularly in the French transactional market. These solutions not only enhance portfolio returns but also contribute to the resilience of energy systems compared to its intermittency.

However, in 2025, France is facing heightened political instability, which is beginning to reflect in the M&A landscape. The regulatory outlook remains uncertain, and upcoming legislative shifts may have a significant impact on investor confidence and transaction dynamics.

Conversely, Greensolver emphasizes that France and the UK still present genuine opportunities for investors. The growing structuring of flexible models, increasing return expectations, and climate goals place both countries at the forefront of the next major transformation in Europe’s renewable energy sector.

Written by Antra Ramboarison

The Latest Renewable Energy News

Webinar Replay – Modeling the Economic Potential of BESS: How to Manage Uncertainty | June 17, 2:00 p.m. CET

Greensolver will be attending the 12th GreenUnivers Infrastructure Financing Conference on July 1

Greensolver at the National Event on “Flexibility in Renewable Energy and Storage” — July 2